题目背景与目标

题目背景:

GAMMA银行是一家私人银行,经营各种银行产品,如储蓄账户、活期账户、投资产品、信贷产品等。该行还向现有客户交叉销售产品,为此,客户使用不同的通信方式,如电视广播、电子邮件、网上银行推荐、手机银行等。在这种情况下,GAMMA客户银行希望将其信用卡交叉销售给现有客户。银行已经确定了一组有资格使用这些信用卡的客户。现在,银行正在寻求您的帮助,以确定可能对推荐的信用卡表现出更高意向的客户。

分析目标:

通过银行收集到的客户属性数据,预测客户是否对当前推出的信用卡感兴趣

资料获取

训练集

测试集

题目描述

分析与实现

特征工程

存在字段ID ,Age ,Region_Code ,Occupation ,Channel_Code ,Vintage ,Credit_Product ,AvgAccountBalance ,Is_Active ,Is_Lead(Target)

很明显,ID字段不可能和目标有任何关系,于是乎直接移除。而地区字段仅仅是RG+数字,于是把RG去除就是Region_Code的数字特征

1

2

| train=train.drop(["ID"],axis=1)

train['Region_Code']=train['Region_Code'].apply(lambda x:x[2:]).astype('int64')

|

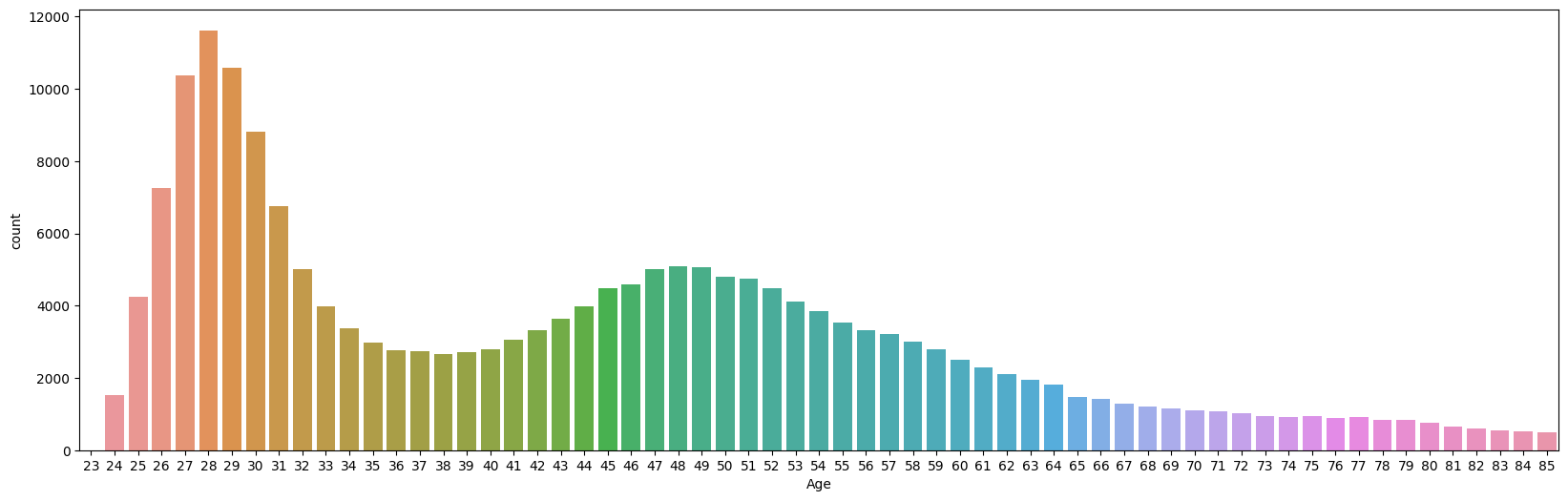

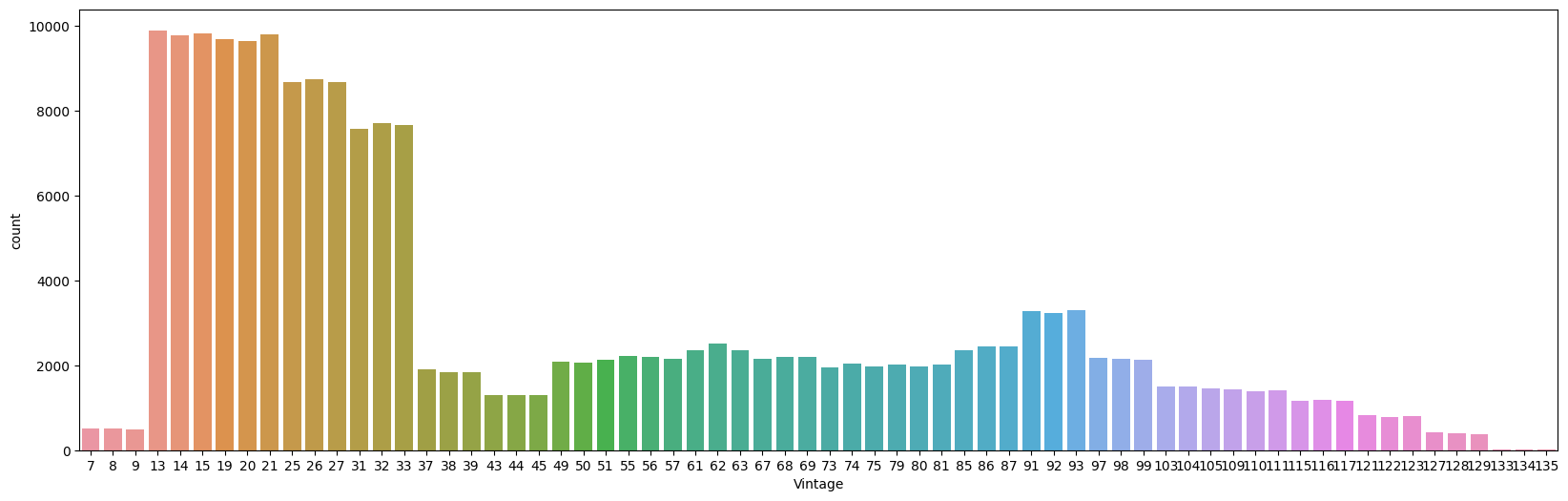

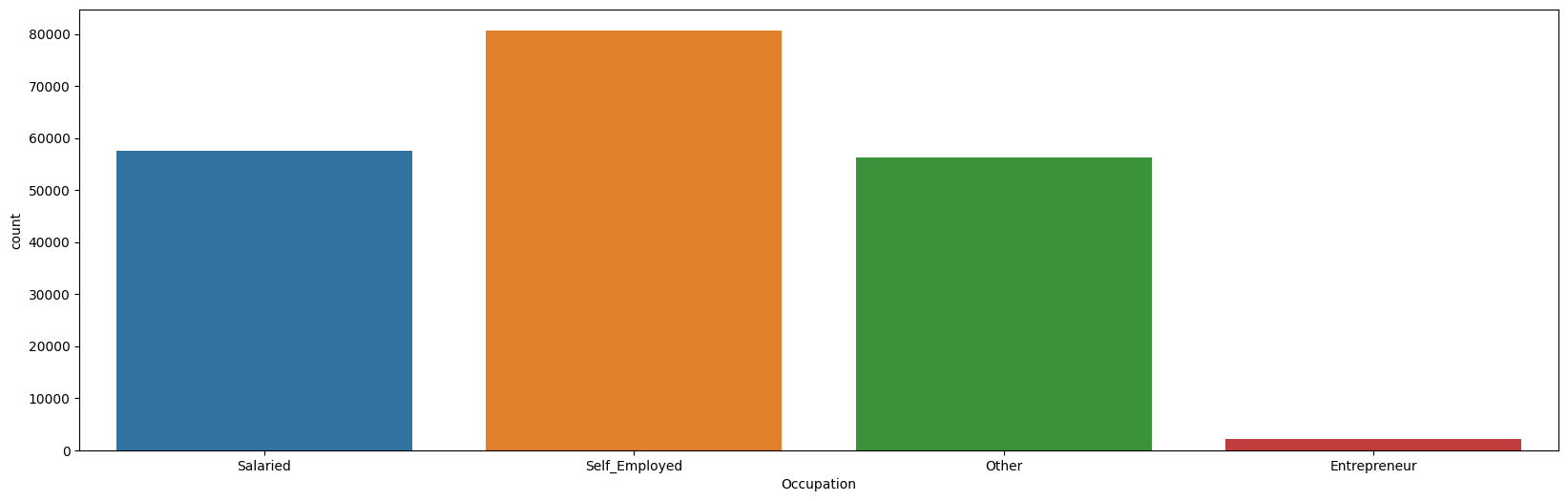

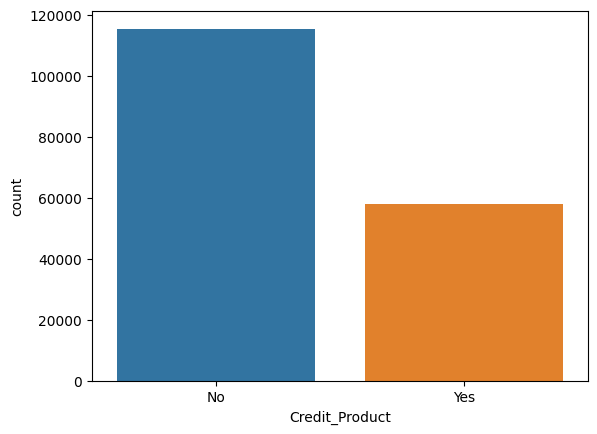

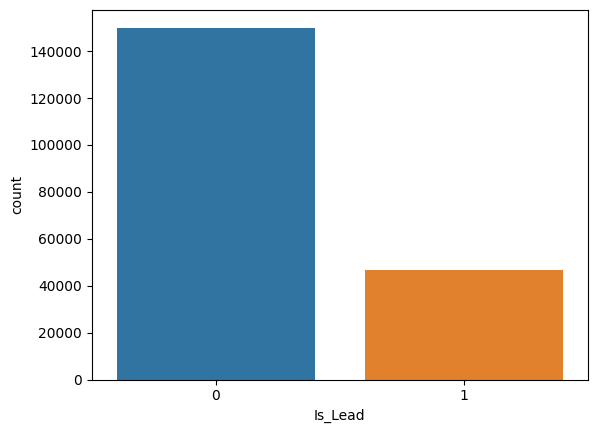

而后,将可能有关系的字段先可视化一下

这两个字段应该也有办法处理一下,但是我不会(´;ω;)

根据图片,需要处理Is_Lead,因为Is_Lead=1的样本量太少了,需要欠采样多数类

1

2

3

4

5

6

7

8

| # 欠采样多数类

df_majority = train[train['Is_Lead']==0]

df_minority = train[train['Is_Lead']==1]

df_majority_undersampled = resample(df_majority,replace=True,n_samples=len(df_minority),random_state=0)

# 结合少数类和过采样的多数类

df_undersampled = pd.concat([df_minority, df_majority_undersampled])

df_undersampled['Is_Lead'].value_counts()

train=df_undersampled

|

首先对字段下为String的部分转换为数字特征

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

|

train["Gender"] = train["Gender"].replace({"Male": 1, "Female": 0}).astype("int32")

train["Is_Active"] = train["Is_Active"].replace({"Yes": 1, "No": 0}).astype("int32")

train["Credit_Product"] = train["Credit_Product"].replace({"Yes": 1, "No": 0})

encoded_data = pd.get_dummies(train["Occupation"], prefix="Occupation").replace({True: 1, False: 0})

train = pd.concat([train.iloc[:, :-1], encoded_data, train.iloc[:, -1]], axis=1)

train=train.drop(["Occupation"],axis=1)

train = pd.get_dummies(train, columns=['Channel_Code'], prefix=['X']).replace({True: 1, False: 0})

column_to_move = train.columns[-5]

column_data = train[column_to_move]

train = train.drop(column_to_move, axis=1)

train[column_to_move] = column_datav

|

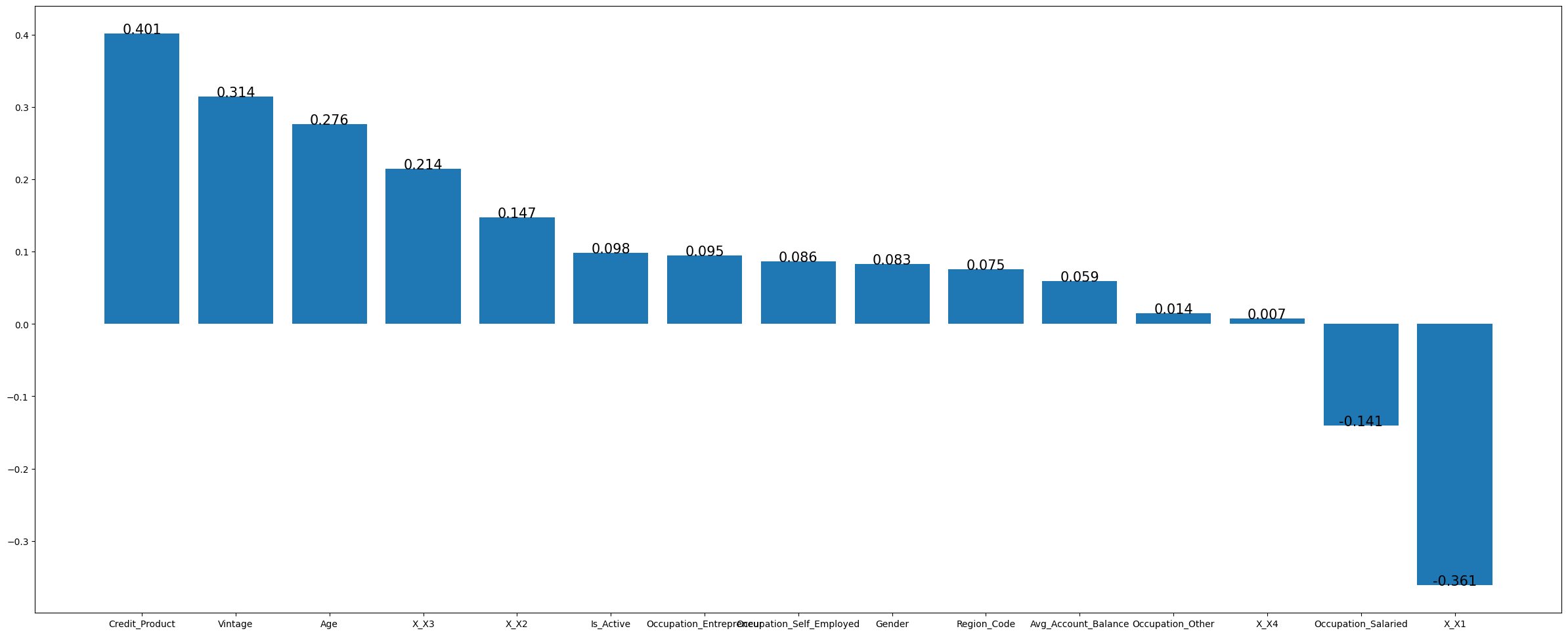

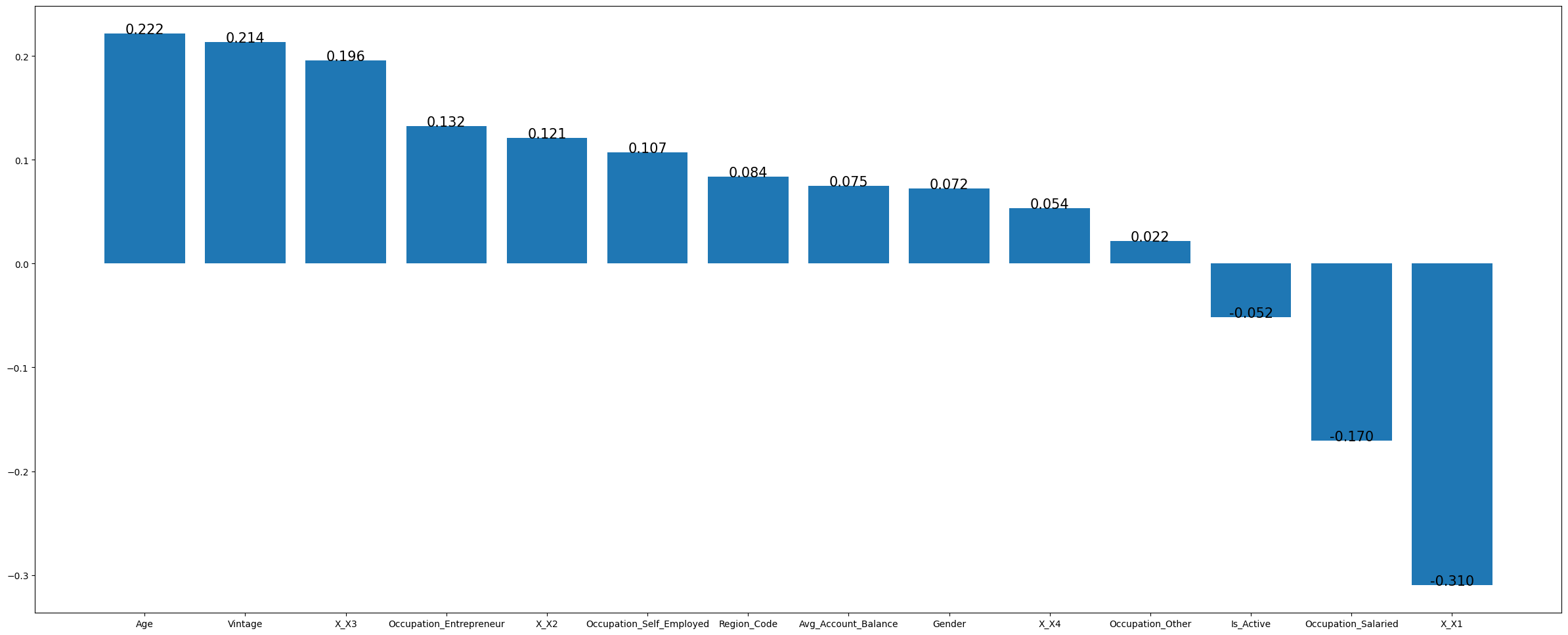

之后打算查看各特征值与是否可能成为信用卡客户的相关性

1

2

| df_corr_lead=train.corr()[u'Is_Lead'].sort_values(ascending=False)

df_corr_lead=df_corr_lead.drop(['Is_Lead'],axis=0)

|

发现Channel_Code ,Vintage ,Credit_Product这三个与Is_Lead关系很密切

那么检查一下是否有缺失吧

1

2

| # 判断是否存在缺失值

pd.isnull(train).any()

|

结果

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

| Gender False

Age False

Region_Code False

Vintage False

Credit_Product True

Avg_Account_Balance False

Is_Active False

Occupation_Entrepreneur False

Occupation_Other False

Occupation_Salaried False

Occupation_Self_Employed False

X_X1 False

X_X2 False

X_X3 False

X_X4 False

Is_Lead False

dtype: bool

|

oops,Credit_Product居然有缺失,它又是和Is_Lead紧密相关,肯定要预测一下

Credit_Product的处理

首先分出Credit_Product的测试集和训练集

1

2

3

4

|

missing_credit_product = train[train["Credit_Product"].isnull()]

non_missing_credit_product = train[train["Credit_Product"].notnull()]

|

然后查看各特征值与是否可能成为信用卡客户的相关性

感觉并没有特别突出的,那就全部训练吧

PS:我尝试对Credit_Product字段也进行欠采样多数类,但是AUC反而变低了,应该是欠采样多数类后样本较少的缘故

1

2

3

4

5

6

7

8

9

|

from sklearn.model_selection import train_test_split

data=non_missing_credit_product.drop(["Is_Lead", "Credit_Product"], axis=1)

x_train,x_test,y_train,y_test=train_test_split(data,non_missing_credit_product["Credit_Product"],test_size=0.2,random_state=22)

from sklearn.preprocessing import StandardScaler

transfer=StandardScaler()

x_train_new=transfer.fit_transform(x_train)

x_test_new=transfer.transform(x_test)

|

模型测试了KNN,逻辑回归、随机森林和lightgbm,lightgbm效果最好

1

2

3

4

5

6

7

8

9

10

11

| import lightgbm as lgb

from sklearn.metrics import roc_auc_score

lgb_classifier = lgb.LGBMClassifier(n_estimators=80, random_state=40)

lgb_classifier.fit(x_train_new, y_train)

y_pred_prob = lgb_classifier.predict_proba(x_test_new)[:, 1]

auc_score = roc_auc_score(y_test, y_pred_prob)

print("AUC Score:", auc_score)

|

AUC Score: 0.7671483718923551

填充好missing_credit_product的值后就开始预测Is_Lead

预测Is_Lead

1

2

3

4

5

6

7

|

data=train.drop(["Is_Lead"], axis=1)

x_train,x_test,y_train,y_test=train_test_split(data,train["Is_Lead"],test_size=0.25,random_state=42)

transfer=StandardScaler()

x_train_new=transfer.fit_transform(x_train)

x_test_new=transfer.transform(x_test)

|

模型依旧选择了lightgbm,但是采用了贝叶斯优化

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

| from bayes_opt import BayesianOptimization

def lgb_cv(n_estimators, learning_rate, max_depth, num_leaves, min_child_samples, subsample, colsample_bytree):

n_estimators = int(n_estimators)

max_depth = int(max_depth)

num_leaves = int(num_leaves)

min_child_samples = int(min_child_samples)

lgb_classifier = lgb.LGBMClassifier(

n_estimators=n_estimators,

learning_rate=learning_rate,

max_depth=max_depth,

num_leaves=num_leaves,

min_child_samples=min_child_samples,

subsample=subsample,

colsample_bytree=colsample_bytree,

random_state=40

)

lgb_classifier.fit(x_train_new, y_train)

y_pred_prob = lgb_classifier.predict_proba(x_test_new)[:, 1]

auc_score = roc_auc_score(y_test, y_pred_prob)

return auc_score

pbounds = {

'n_estimators': (150, 220),

'learning_rate': (0.02, 0.09),

'max_depth': (10, 15),

'num_leaves': (20, 100),

'min_child_samples': (5, 50),

'subsample': (0.5, 0.7),

'colsample_bytree': (0.6, 1.0)

}

optimizer = BayesianOptimization(

f=lgb_cv,

pbounds=pbounds,

random_state=42

)

optimizer.maximize(init_points=10, n_iter=100)

best_params = optimizer.max['params']

best_auc = optimizer.max['target']

print("Optimal Hyperparameters:")

print(best_params)

print("Best AUC Score:", best_auc)

|

超参数:

‘colsample_bytree’: 0.610865775300284

‘learning_rate’: 0.0805284415086373

‘max_depth’: 13.707039129713081

‘min_child_samples’: 7.262616569392997

‘n_estimators’: 215.9489533887009

‘num_leaves’: 87.00033587605007

‘subsample’: 0.620344288616325

Best AUC Score: 0.8755665739616039

后记

这个题给我的感觉是特征工程比较重要,最开始选择把Credit_Product填为平均值0.333333,没有进行任何其他操作,效果很差劲,进行预测之后,虽然AUC仅仅0.76,但是对于最终AUC提升还是比较明显的

源码